Without any specific plan in place, such as how you’ll qualify for Medicaid or a long term care insurance policy, you are said to be self-insured for long term care events. Recent studies have shown that up to 80% of women aged 65 and above and 60% of men in the same age category will require long term care at some point in their life.

Given that the average annual cost for semi private nursing home is over $93,000 and the median annual cost for home care is $55,000, you’ll want some plan in place to help prepare you for the financial implications of long term care.

Even one spouse suffering a long term care event that requires a nursing home stay can decimate a couple’s retirement savings. Scheduling a consultation with an elder law attorney is your best opportunity to get questions asked about long term care insurance and other opportunities for funding these potential medical needs.

While no one wants to find themselves in the position of unexpectedly paying for nursing home care, this happens all too often. You’ll want to speak directly with an elder law attorney who can help you work through the connections between your estate plan and your long term care plan.

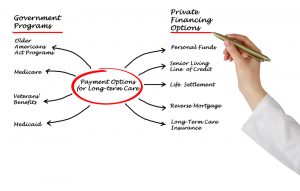

individuals. You may pay with three primary sources; family, self-insuring by paying through out of your own pocket, or a long-term care insurance.

individuals. You may pay with three primary sources; family, self-insuring by paying through out of your own pocket, or a long-term care insurance.

5

5