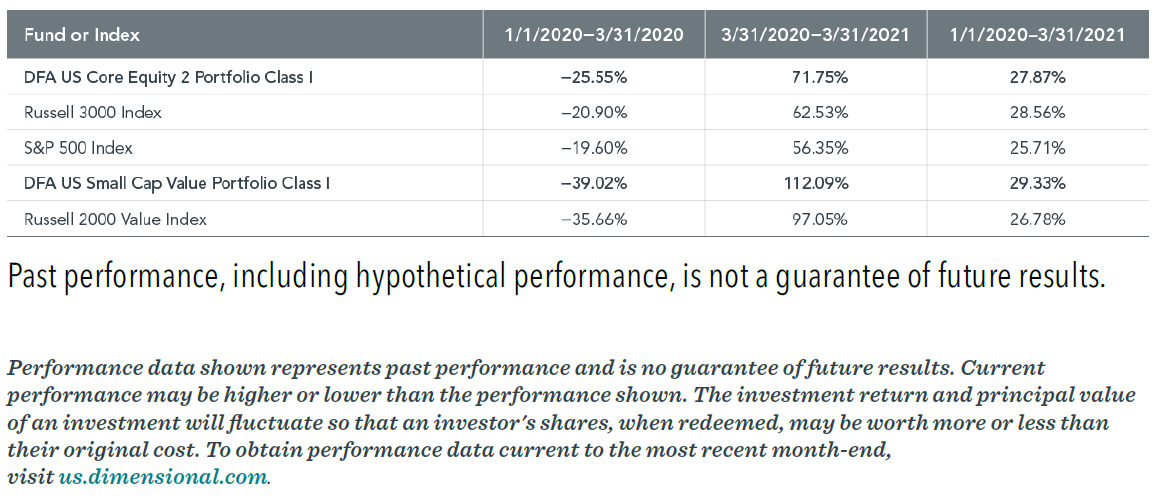

A year ago, at the end of March 2020, the S&P 500 was down nearly 20%1 and the world was scrambling into lockdown. Many experts wrote articles telling us where we would be in a year. I don’t remember reading any that said the S&P 500 Index would be up 56% over the next 12 months. But that’s what happened.

I didn’t predict any of that. I never do. Last June, I spoke about the Old Normal and how we should be prepared for market downturns once or twice a decade, while accepting we just can’t know when they’ll happen. We can’t predict financial crises, but we should plan for them. That’s why I always recommend having a trusted financial advisor, a fiduciary who puts your interests first, who can help you understand the range of possible outcomes and create a plan tailored to your goals and acceptable levels of risk.

If you stayed in the market, it might be time for a victory lap. Dimensional’s US Core Equity 2 Portfolio, which holds a diversified mix of broad US equities and is Dimensional’s largest core portfolio, returned nearly 72%, as Exhibit 1 shows. Within the US market, small cap value stocks2 were among the hardest hit. Dimensional’s US Small Cap Value Portfolio was down 39% in the first three months of 2020 and subsequently returned a showstopping 112% over the next 12 months.

Sticking to long-term investment plans in the face of such extreme uncertainty wasn’t easy. I have so much appreciation for what the financial advisors we work with went through to keep their clients in the market, and nothing but admiration for what they achieved.

We were all stressed out last March. There was pressure to “do” something, to make changes just for the sake of reacting. People might get out of the market in an effort to reduce uncertainty. But getting out of the market can actually increase uncertainty because it can force investors to make a difficult decision: choosing the best time to get back in.

This highlights something I’ve long believed to be true: while all investments have risk, many people who think they’re investing are actually gambling. It is a really simple distinction for me; if you’re trying to time short-term market movements, you’re gambling.

Staying focused on a long-term strategy during times like the past year is hard work. Short periods like the first quarter of 2020 and the past year are not signals of future performance, but reminders of just how hard being a long-term investor can be. We didn’t know returns like that would come this year, but we knew we needed to be in the market to capture them when they do show up.

As I’ve said before, every crisis is different, but I think the best way to deal with them is always the same. We can’t control crises, but we can control our response to them. You want to be prepared to deal with the unexpected before it happens. Not when you’re stuck in the middle of it.

What is the Next Normal? It’s expecting uncertainty and committing to a plan that addresses it. It’s rising above the temptation to make changes when things get tough. It’s understanding the difference between investing and gambling. And it’s remembering how good it feels when things work out according to plan.

If you don’t already have a plan that includes crises among the range of possible outcomes, it’s never too late to create one. This is not the last crisis any of us are likely to experience. If we make thoughtful planning the New Normal, we’ll all be ready for the Next Normal.

By: David Booth

Executive Chairman and Founder

References:

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission. Consider the investment

objectives, risks, and charges and expenses of the Dimensional funds carefully before investing. For this and other information about the

Dimensional funds, please read the prospectus carefully before investing. Prospectuses are available by calling Dimensional Fund Advisors

collect at (512) 306-7400 or at us.dimensional.com. Dimensional funds are distributed by DFA Securities LLC.

Investing risks include loss of principal and fluctuating value. Small cap securities are subject to greater volatility than those in other asset

categories. These risks are described in the Principal Risks section of the prospectus.