Not all assets belong in a trust, and knowing the difference can help you make the right choice for your assets. The easiest way to figure out whether or not a trust can help you is to sit down with your lawyer and make a list of all the assets you own.

There are several types of assets commonly transferred into trusts. These include: life insurance policies, antiques and collectibles, business interests, investments and money market accounts, deposits inside credit unions and banks, realy property, and stocks.

The trust is only formally set up when you take these assets and transfer them into the ownership of the trust itself. It is at this point that these assets are truly owned by the trust and under the management of the trustee you have chosen.

Since trusts offer a lot of benefits, using one is a common way to ensure you’ve considered all your estate planning issues across the board. Benefits include passing on your assets without having them go through probate, putting aside certain assets for the care of someone in your family with special needs, establishing requirements for beneficiaries to meet before assets will be distributed, and creating a plan for managing your business or personal assets.

With many trust tools out there, it’s important to be well-informed. Not all trusts are created equal. Deciding what’s right for you and your intentions might look different from your neighbor or coworkers. Sitting down with an attorney in New Jersey who has experience in estate planning and using trusts will give you a better perspective on how to best leverage these tools.

Planning ahead for potential incapacitation, Medicaid use, and estate planning all feel inherently personal. In fact, they hit so close to home that plenty of people never even begin the process of estate planning.

But for those who do, the planning is often the first and last step they take. A study recently found that most heirs have no idea what their loved ones intend to do with assets. Among those who said they hadn’t told their family members about estate plans, 10 percent reported that it wasn’t anyone else’s business what they chose to do with their assets.

But holding your cards close to your chest like this could backfire in the heat of the moment. Various old copies of wills, verbal agreements to give a certain loved one a treasured piece of art, and sibling rivalry can all lead to additional confusion and even decimation of the assets you’ve worked so hard to build over your life.

In total, at least sixty-four percent of people stated in the study that they’d never talked with their family members about estate planning. Most of those respondents shared that their estates and assets would be divided equally among their heirs, whereas others used different criteria to decide who would get what.

Most families take the top-down approach, with the person who holds most of the assets being the sole decisionmaker when it comes to what happens to those items and the money. If you intend to keep your estate as private as possible, consider sharing your plans and key documents with your estate planning attorney so that someone in the know has access to this information during a crisis, such as if something happens to you unexpectedly. Talking to an attorney can provide you with further information on tools to use and how often to update your material.

You might have heard the term pour-over will while discussing the

possibility of a revocable living trust with your estate planning lawyer. A

living trust is often used in conjunction with a pour-over will.

The essence of how this works is that all property that passes through your will at the time of your death is transferred into a trust and is then distributed to trust beneficiaries that you named while you are still alive. Many people might be curious about whether or not there are advantages to using a pour-over will.

What’s the reason for having a will that does nothing except transfer property into your trust? The answer is that your estate planning attorney might recommend that it’s a good idea to have all of your assets protected by the terms of only one document and that is your trust document.

There are three major advantages to using this pour-over will. First of all, trusts are private unlike a will. Secondly, you won’t transfer everything you own into your living trust, but the pour-over will gives you a sense of completeness because it takes care of assets that you don’t get around to transferring into the trust prior to your death.

Finally, the last advantage of a pour-over will is simplicity. It makes it extremely clear as to who receives what and, therefore, makes that process simpler for your trustee and executor, who are responsible for wrapping up your estate after you pass away.

A power of attorney document is instrumental in outlining who is

eligible to step in and manage your finances if you become unable to do so.

Unfortunately, far too many people make mistakes in the process of creating a

financial power of attorney. While this document doesn’t need to be difficult

or complicated to make, it is critical that you do it properly with the help of

an experienced estate planning lawyer.

There are six major mistakes that can be made in your financial power of

attorney, many of which can be completely avoided by sitting down and working

with an estate planning lawyer who has extensive experience in the creation of

these documents. These common mistakes include:

Not giving authority over all types of your property. You might want to provide a comprehensive list or specify which type of property they are eligible to make decisions about.

Not enabling your financial institutions to work with you in advance. Make sure that you have filled out the paperwork to the specifications of these banks or credit unions.

Making your agent the joint owner of your bank account.

You might have heard the term pour-over will while discussing the possibility of a revocable living trust with your estate planning lawyer. A living trust is often used in conjunction with a pour-over will. The essence of how this works is that all property that passes through your will at the time of your death is transferred into a trust and is then distributed to trust beneficiaries that you named while you are still alive.

Many people might be curious about whether or not there are advantages

to using a pour-over will. What’s the reason of having a will that does nothing

except transfer property into your trust? The answer is that your estate

planning attorney might recommend that it’s a good idea to have all of your

assets protected by the terms of only one document and that is your trust

document.

There are three major advantages to using this pour-over will. First of

all, trusts are private unlike a will. Secondly, you won’t transfer everything

you own into your living trust, but the pour-over will gives you a sense of

completeness because it takes care of assets that you don’t get around to

transferring into the trust prior to your death. Finally, the last advantage of

a pour-over will is simplicity. It makes it extremely clear as to who receives

what and, therefore, makes that process simpler for your trustee and executor,

who are responsible for wrapping up your estate after you pass away.

It’s been said that your estate plan is only as good as the agents associated with it. It’s important, for example, to have conversations around the family’s intentions, especially between spouses.

Wives and husbands should both be involved in creating final documents to help avoid unnecessary or unforeseen complications during the most challenging of times for your family. It’s important for you and your spouse to be comfortable with other professional advisors in your life, including an attorney, an accountant, and a financial advisor.

Many spouses might stop here, tempted to keep the details of their

estate plan to themselves. However, the communication of the estate plan to any

involved children is critical. It’s all too easy in our American culture to put

off these discussions due to the potential for conflict. However, taking

necessary steps to discuss your intentions with your family members can make things

easier if you were to become incapacitated, or if you or your partner were to

pass away unexpectedly.

It is important to overcome your short-term hesitations about having conversations on your estate plan for the more long-term benefit of having a clear plan in place that minimizes the potential for disputes.

Every family has their own distinctive dynamics, but providing a deeper understanding of your intent and the estate planning steps you’ve already taken can make things easier for your family members during what will otherwise be a challenging time as they attempt to negotiate the financial and legal steps of caring for you during a time of incapacitation or assisting with family through your recent passing.

Nearly half of all Americans have no estate plan at all, so you’re to be commended if you’re ahead of that curve. But once you’ve dotted all the I’s and crossed all the t’s, it’s time to make sure you’ve secured these documents so that you or a trusted advisor can access them in the event of an emergency.

Your estate planning attorney might be able to help you

store your documents, but have a conversation about this first to ensure you know

what’s happening to your materials. Most law firms today use fireproof, locked

file cabinets. Sometimes an offsite storage facility might also be used if your

law firm is located in a big city.

Although most people still want their attorney to hold on to

the original documents, this does not mean this is your only option. Some

lawyers have turned to providing clients with the originals due to security or storage

space concerns. Most people might consider a safe deposit box as the first

place to put something like your powers of attorney and will, but the ability

to get into such a box is limited. If something happens to you, another person

will have to get court authority in order to access the box. And most likely

your loved ones can’t get that court authority because the documents to show

their rights are in the box.

A fireproof safe is a great way to protect your key

documents and ensure that you know where they are at all times. The safe is the

right place to keep the originals and you can store other copies elsewhere. Go

back to review your documents on a regular basis and make sure to update any

originals in the safe as well as where you’ve stored copies if you make big

changes or replace a document entirely.

Whether you’re married, single, or remarried, you’ve got to have an eye

towards your own future as a female. Estate planning, financial planning, and

asset protection planning are all part of your retirement strategy and connect

with how you’ll support yourself in your golden years.

Many women have to look decades beyond their retirement when it comes to

their plans given data on longevity and forecasts about the expense of

long-term care.

A recent study incorporating insights from high net worth earners found that women ranked themselves highly on their ability to perform a range of financial tasks but diverged from men when it came to their top two current financial goals. Executive women reported that their top goal was to know that they were prepared for the worst and planning for retirement. However, male executives said that providing for future generations and taking care of their dependents financially were two of their top three financial goals.

Plenty of women today recognize that they might live longer than their

male partner, or that they could be affected by the phenomenon of grey divorce

which would significantly impact their retirement planning goals. Furthermore,

women might be recognizing the possibility of needing long term care support

which can be quite expensive and can decimate an otherwise carefully crafted

retirement plan. If you want to look ahead into the future to prepare yourself

for your estate and the possibility of long-term care, schedule a consultation

with an experienced estate planning lawyer today.

Heading off into your financial future without a clear plan and goals is like setting sail without charting your course first. It’s one of the biggest reasons why people feel anxiety over their finances; lack of a plan.

A recent study completed by the Financial Planning Association shows

that more than 60% of respondents in a recent study indicated very high levels

of negative stress in their life. Furthermore, more than 20% of people who

participated in the study said that their stress levels have increased over the

course of the past year and more than 30% said that their stress levels have

jumped over the last five years.

Prioritizing financial goals and establishing a plan for debt management

are some of the most important things that you can do to experience feelings of

financial security and lower your stress levels. The study found that nearly

three quarters of survey respondents who said they felt clear about their overall

financial goals have lower stress levels.

One way to evaluate your current expenses are to assign time frames to

your goals, such as short term, medium and long term. Your financial goals can

also include looking ahead to the future to establish goals for estate, asset

or even business succession planning. A consultation with an experienced

attorney can go a long way in helping you to clarify what you intend to

accomplish with your financial goals.

The law enables you to use tools such as trusts and wills to accomplish your goals and provide for the people you care about either during your life or after you pass away. While these are definitely protective tools to begin with, there are unfortunately many people who see themselves as opportunists who use these tools to try to take advantage of others, especially seniors who might be experiencing cognitive decline.

The targets of these kind of schemes are often those people who have

significant assets who are vulnerable due to memory issues, advanced age

concerns, illness, or family isolations. Family members who might have been

expecting an inheritance from a loved one could even be surprised that they are

cut out of the will entirely or received much less than they anticipated

because another party has exerted undue influence on your loved one.

If a person has received a substantial benefit from a trust or a will

and had a confidential relationship with a person who created it and is also

active in procuring this gift, this could lead to a presumption of undue

influence. This could be a formal fiduciary relationship or an informal trust

relationship in which the influencer exerts his or her impact to get the person

to include them in the will to make a gift or update their trust such that the

influencer is the beneficiary. Being knowledgeable about undue influence and

how it can potentially impact your estate is important.

Many people are already familiar with the 2017 Tax Cuts and Jobs Act that made significant changes to tax planning. However, the gift tax and estate tax exemption should be something that you’re familiar with so that you can leverage these to your advantage. It’s important to understand that the 2017 tax reform pushed up the maximum exemption to what is essentially double the previous amount.

However, with regards to your tax and estate planning, this change is

not permanent. By 2026 the exemption will drop down to 2017 levels unless

Congress decides to make changes prior to this time. Other plans to reevaluate

the exemption level have been put on pause for this moment but it is very likely

that Congress will at least reconsider the issue in the near future.

If you already have a taxable estate, it is important that you do not

just file this information away. Instead you should begin to take action

immediately. For planning of this scope and size, it is critical to work with a

team of knowledgeable professionals to assist you with your tax and estate

planning concerns.

A certified public accountant, a financial advisor, and an estate

attorney are just a handful of the people who can help you understand how you

might be currently affected by estate planning and tax planning concerns and

how future issues could require you to update your plan all over again.

Schedule a consultation to sit down with a knowledgeable attorney today so that

you can figure out what makes the most sense for you personally.

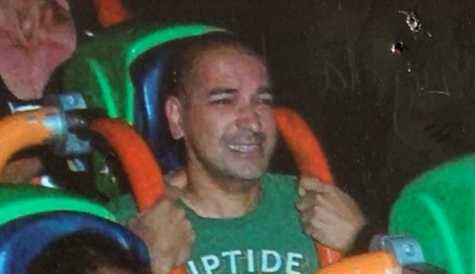

Check out my face in the image above. Am I smiling? Crying? Scared or excited?

This picture was taken at Kingda Ka at Six Flags Great Adventure in New Jersey. It was about 5 years ago; this is one of those pictures that the amusement park sells you that’s taken as you are on the ride (I’ve cropped out the friends & family to avoid making them angry).

It is said FEAR and EXCITEMENT is same emotion, just +/- CONFIDENCE. There’s a part of me that’s smiling on this ride because I am confident that the orange harness and the seatbelt are going to keep me in my seat and deliver me back safely to the platform. Let’s just say I wouldn’t have that same smile if I didn’t have that level of confidence.

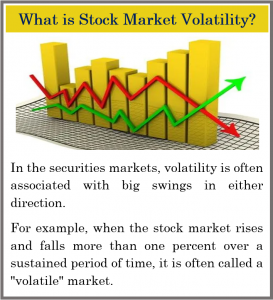

On August 5th, 2019, the Dow Jones Industrial Average had its worst fall of 2019. Were you smiling or crying? How about inwardly? Was your stomach in knots? I suppose the answer to that depends on your level of Confidence. Volatility & risk are not the same thing. When a stock is volatile, it means that it tends to make big moves (up or down). When a stock is risky, it means it can lose money (go down). In financial terms, risk is the potential permanent loss of money. Whereas volatility is how rapidly an investment tends to change in price.

When equity markets experience unnerving fluctuation, we suggest you ask yourself 3 questions:

1. Have my financial timelines changed?

2. Have my financial goals changed?

3. Has my risk tolerance changed?

If you’re not sure or if you answered “yes” to any of those questions, then it’s time to have a conversation with your Advisor. The goal is to give you confidence that you’re taking the right amount of risk. And depending on your concerns, it may be time for a review of your financial plan, revisiting your risk tolerance, investigating your diversification, as well as other strategies.

And then – strap in and enjoy the bumpy ride. Get to the point where you’re smiling and can enjoy it because you know you’re going to get delivered to your platform safely. And if we can help deliver you, feel free to reach out.

When creating your will, it’s natural to be concerned about deciding specific pieces of property or assets that will pass on to the loved one or beneficiary you decide. However, all too many people approach the process of putting together a will in a far too simplistic manner, exposing them to potential challenges or even their loved ones to potential issues in the future.

It’s important to find an attorney that you can trust to work with on your

estate plan so that you can avoid many of the most common mistakes that end up

following your loved ones into the future. Specific bequests inside a will are

managed first in the administration of your estate and the person who passed

away may not even own that investment anymore. The estate could be required to

purchase an investment at a higher price which could harm beneficiaries if you

name the specific investment in your will. Here is a great example of how this

could turn into a significant problem. If you leave behind shares of a

particular stock, which at the time of creating the will is worth a specific

amount of money, such as $5000, the same number of shares could increase in

value significantly at the time of your death and those shares might not be

owned by you anymore. The estate would then have to purchase those shares and

pass them onto a grandchild and this could use essentially all assets inside

the estate such that future beneficiaries get little to no assets. Sit down to

speak with your estate planning attorney about how to make your estate work for

you and how to avoid these kinds of issues.

During volatile times, many investors get agitated and begin to question their fundamental investment decisions and choices. This is especially true for those investors who monitor their portfolios daily and can be tempted to pull out of the market and wait on the sidelines until it seems safe to dive back in. One thing that can be helpful is to understand that equity market volatility is part of the investment experience and is therefore inevitable. Equity markets can always move up and down, especially over the short-term. Some suggest that the only certainties in life are death, taxes and market volatility.

Trying to time the

market can be extremely difficult. One solution is

to always understand your personal situation. Try to plan for your equity

investments to maintain a long-term horizon and ignore the short-term

fluctuations. To help make your investment decisions less emotional and

more focused it is helpful to understand volatility. If the daily swings in the stock market seem

too chaotic, remember these movements are near impossible to fully predict. For

many investors there is no reason to even subject themselves to daily market

headlines. If you have a long-term investment horizon for your equity holdings

of at least five years, chances are the current volatility will pass – possibly

in a couple of weeks, months or in at least a couple of years.

Try to keep things in

perspective. Market pullbacks

(defined typically as between 5 and 10%), corrections (defined as 10 to 20%) and

even bear markets (defined as 20% or more) are a normal part of the stock

market cycle. According to Guggenheim, since 1945, the S&P 500 has declined

between 5% and 10% 78 different times. The average time it took to recover to

its previous highs was only about one month.

(Source: US News and Money Report 6/7/2018)Volatility and risk are not the same thing. When a stock is volatile, it means that it tends to make big moves (up or down). When a stock is risky, it means that it can lose money (go down). In financial terms, risk is the potential permanent loss of money whereas volatility is how rapidly an investment tends to change in price. Volatility does not just imply risk of loss. Volatility simply refers to the price action. Some investments may be more volatile than others. Equity investments as a category are much more volatile than a bank deposit, but that does not mean an investor should avoid investments in equities. Just because an investment is more “volatile” does not necessarily mean it is “riskier” in the long term. Investors should always discuss with their financial advisors the potential of short-term volatility affecting the daily value of their investments and plan their investments accordingly

Short-term

movements of the market are unpredictable and do not abide by any average

Equity

markets are never going to produce straight line returns for investors. For example, in 2017, the stock market had an

unusual year in which it did not even deliver a correction of 5%. Meanwhile, 2018

brought investors the steepest correction in a decade during the fourth quarter

and that year included a greater than 10% decline in the first quarter.

At any time, the equity markets could see a retreat of 10% or more which is referred to as a market correction. Here are four facts that can help investors understand market corrections.

1. Corrections are a part of the investing experience.

Since 1950, the S&P 500 has undergone 37 separate stock market corrections of at least 10%, not including rounding (i.e., declines of 9.5% to 9.9%). Considering that there have been over 69 years since the beginning of 1950, this works out to a correction, on average, every 1.87 years. (Source: The Motley Fool 5/2019)

2. The average length of those corrections was about 6 months.

According to data from stock market analytics firm Yardeni Research, the S&P 500 has spent 7,135 calendar days in correction since the beginning of 1950. Since then, there have been 37 corrections (of at least 10%). This works out to an average resolution time of 192 days, or slightly more than six months. Of these 37 drops in the market, 23 of them have resolved in 104 or fewer days, with only seven lasting longer than 288 days. 11 of the 14 instances that lasted longer than 104 days occurred between 1950 and 1984. (Source: The Motley Fool 5/2019)

3. “Rally” days outnumber correction days 2.55-to-1 since 1950.

Since the beginning of 1950 until May 13, 2019, there have

been a total of 25,335 calendar days and over 69 years of data. During this

time span, the S&P 500 has spent 7,135 of those calendar days tumbling from

a peak to a trough. This means that for the other 18,200 calendar days, the

S&P 500 has spent its time rallying from these correction lows. This ratio

of upward momentum (18,200) to correction (7,135) is a healthy 2.55-to-1.

(Source: The Motley Fool 5/2019)

Key Points

1. Market volatility is not the same as market risk. 2. Corrections are a part of the investing experience. 3. Beware of media magnification 4. Avoid making emotional decisions 5. Focus on your personal goals and call us with any concerns.

Big up days occur within two weeks of big down days 60% of the time.

J.P.

Morgan Asset Management releases an annual report

titled, “Staying Invested During Volatile Markets.” This report looks

at the S&P 500 over the trailing 20-year period and calculates what an

investor would have made had they stayed invested, rather than trying to time

the market by jumping in and out when they saw the first signs of trouble.

Oftentimes, missing the S&P 500’s 10 best days means losing more than half

of your would-be 20-year returns, missing around 30 of the best single-session

gains, resulting in a loss over the 20-year

period. (Source: The Motley Fool 5/2019)

An

interesting observation in this annual report is the timing of when these worst

days and best days occur. Although it has varied slightly from report to

report, since the trailing 20-year dates being analyzed are changing, roughly

60% of the S&P 500’s top single-session gains occur within two weeks of its

10 largest single-session losses. This means that selling equity positions

during big down days may cause you to miss out

on the market’s biggest single-day rallies, which are impossible to time.

Beware

of Media Magnification

One of the

biggest challenges investors face is how to tune out the magnification of

financial issues by the media. With thousands of media outlets all

thirsty for viewers, some outlets resort to scare and fear tactics to attract

an audience. Know that volatility is a part of the investment experience,

however, it can still become difficult to make rational investment decisions

when the markets are fluctuating. During these times, it is prudent to resist

the temptation of watching news reports and obsessively watching your portfolio

performance. Adhering to a long-term investment plan often requires taking the

news with a grain of salt and putting spur-of-the-moment advice of others on

the back burner.

Too

often emotion, not logic, can overshadow investing habits, so the first step in

declaring this mental independence is realizing how these influences, known as

biases, affect us. Sometimes, the closer

you put a short-term lens to your investments, the more likely you consider

decisions that deviate from your long-term strategy.

What

should an investor

do in a volatile market?

In times of crisis, many people tend to overreact and sometimes do not make the

best decisions. During volatile markets, it might be best to revisit your

plan. Remember panic is not a plan.

When equity markets

experience unnerving fluctuations, we suggest you ask yourself three questions:

Have my financial timelines

changed?

Have my financial goals

changed?

Has my risk tolerance

changed?

If you answered “YES” to any

of these questions, then it is wise to discuss these changes with us. An

investor needs to be prepared to build a plan that includes risk

awareness. One of our primary

responsibilities as your financial advisor is to consistently keep in touch

with you and monitor your situation. If

you have concerns, some questions to ask us include:

Can we review my financial plan?

Can we revisit my risk tolerance?

Are my investments diversified?

What are my fixed income investments?

Has the volatility presented any good opportunities?

While equities have risen, the continuing backdrop of a weakening

economy, trade war fears and interest rate concerns always offer the

opportunity to recheck your plan. Today’s traditional fixed rates might not

help many investors to achieve their desired goals, so most investors may still

need to include a strong mix of equities. Markets can continue to rise but they

also could head lower.At the end of the day,investors

should always put their primary focus on their own personal goals and

objectives. If anything has changed for

you please let us know.

Let’s focus on YOUR

personal

goals and strategy.

Our primary objective

remains to continually understand our client’s goals and to match those goals

with the best possible solutions.

Our advice is not one-size-fits-all. We will always consider your

feelings about risk and the markets and review your unique financial situation

when

making recommendations. If you would like to revisit your specific holdings or

risk tolerance please call our office or discuss this at our next scheduled

meeting.

We pride ourselves in

offering:

consistent and

strong communication,

a schedule of

regular client meetings, and

continuing

education for every member of our team on the issues that affect our clients.

A skilled financial advisor can help make your journey easier. Our goal is to understand each of our client’s needs and then try to create a plan to address those needs. Should you need to discuss your investments, please call our office.

If you’re like most parents, completing that to-pack for college checklist can seem completely overwhelming. But as you get closer to the finish line, it also becomes a challenge to think about how your life- and your student’s life- will change.

For those students on their own for the first time ever, there are a lot of changes around the corner for them. Things they might not have had to think about before, such as what happens if they get into an accident on or around campus? What happens if they need medical attention? Who is allowed to make medical decisions for them?

While you as the parent have served in that primary role for a long time, remember that if your student has hit age 18 and is moving out to attend college that decision-making power does not automatically default to you.

If your child is out of state at college, make sure you add one last thing to your “must-do” list: a healthcare power of attorney. In addition to packing a copy of the health insurance card and important phone numbers your child might need while away at school, it’s key to have these documents created before they go.

While no parent wants to think about something happening to their student, it’s not that difficult to set up a plan to protect them in the event of an emergency. A properly-drafted plan ensures that you get a phone call when something happens to your student on campus and that you can, legally, be brought into the situation to help make medical decisions.

Far too many students head off to their new campus dorms without thinking twice about this issue. While for many the need for a healthcare directive won’t be an urgent matter, it’s worth having that plan in place just in case something happens. Remember, your 18 year old now legally has the right to make decisions, including those related to medical care, on their own- if you’d still like to be involved, make sure you set aside some time to talk about a healthcare directive that will give you peace of mind after they move in.

One of the reasons we don’t do our financial planning, tax planning or estate planning, is because we don’t really feel moved by the possible future. A Harvard business report (which you can find here) showed that people will make better decisions when they stopped seeing their future selves as “strangers.”

I was reminded of this as I played with the FaceApp, which has been making it’s way around social media lately. (Yes, I am aware that the Russians may now have my likeness, but I’m pretty much everywhere on the Internet anyway, why not one more place? I’ve since deleted the app anyway.)

It was eye-opening to see what I may be looking at in the mirror 30 to 40 years from now. In fact, I also found it insightful to see what the app had to show for my likeness 30 years ago. What kind of legacy do I want to leave behind? What is 83-year-old Neel trying to say to 43-year-old Neel? And for that matter what does 43-year-old Neel want to say to 13-year-old Neel? What about you? What would you tell yourself you get the opportunity speak to yourself 30 years ago? What do you want your legacy be? And how we accomplish that? That’s where we can help. If we get together I would love to hear your goals, dreams and wishes. Maybe that person in the picture doesn’t have to be such a stranger.

Finally, we celebrated my mother’s birthday over the weekend. My maternal grandfather (Dada) sat next to me at dinner. We decided to use my FaceApp picture and do a side-by-side with his picture. Check it out below. Made me think – maybe I didn’t need the app after all. Feel free to reach out if you want to chat about your future, present and/or past.