If you own an entire property in New Jersey or a portion of a property in New Jersey but live outside the state, there are several important things you need to recognize about the process of passing this on to someone else. First of all, New Jersey does not have a state gift tax.

At the federal level in 2020, however, there is an annual federal gift tax exclusion of $15,000, meaning that any gifts extending beyond that amount require you to file a gift tax return for the portion above $15,000. It’s also important to recognize your overall lifetime estate tax exemption which is $11.58 million for individuals in 2020. No gift tax would be incurred as long as you do not intend to make gifts greater than that amount.

Although it seems like with little tax implications there is good reason to make this gift during the course of your life, the purchaser’s cost will carry over to the recipient of a gift, meaning that your child could inherit the property with a cost basis equal to whatever you paid for that share of the property or the property itself. If the property has increased in value significantly since you purchased it, this means that you could be subjecting your child inadvertently to a large capital gain tax.

Some other states, such as Pennsylvania will have a reciprocal income tax agreement with New Jersey but this does not extend to income that goes beyond compensation. For more information about some of the challenges associated with passing on property, schedule a consultation with a trusted New Jersey lawyer today.

Planning for an estate is important for everyone, but especially if you are the caretaker of an adult with disabilities, it’s important to ensure all the documents are lined up to protect this person. The guidance of guardianship estate planning statutes can enable a court-appointed guardian of a disabled adult to put together estate plans for those adults based on a petition to the court. Across the U.S., there are thirty-two states with provisions on the books that enable estate planning to be formally handled by a guardian on behalf of a disabled party.

While these 32 states do have laws on the books about these issues, those statutes usually fall into two general categories. For the first set of states, statutes allow guardians to have broad power over estate planning issues on behalf of a disabled adult.This can include carrying out trusts, codicils, and wills. Only a handful of these states, however, allow the guardian to actually make the will on behalf of the disabled party.

The second grouping of states include those that have either left out of the power to make the will in an implied or expressed manner. This means that the ability to make a will is either not mentioned or has been expressly prohibited as something that a guardian can do on behalf of any adult with a disability.

Estate planning is not always a power that an appointed guardian can do for a disabled adult. This includes creating a will but also incorporates other kinds of estate planning powers.

If you are interested in being appointed as a guardian for an adult in your family who lives with disabilities, it’s important to sit down with a trusted estate planning attorney to discuss your options. Knowing exactly what you can and cannot do when appointed in this role will give you some clarity and allow you to accomplish what is needed on behalf of an adult with a disability. Need more help? Our NJ estate planning law office is here to help you.

As a result of Covid-19, many people are thinking about estate planning and financial planning in a whole new different way. Having difficult conversations about end of life and long term care plans has become top of mind for many families who might have had to confront these issues directly.

Even if you’ve maintained your health and your family during this crisis, it’s a good opportunity to step back and plan for your own future. Incapacity planning and updating your estate should be some of your biggest priorities.

Having a loved one diagnosed with Covid-19 or having to prepare loved ones for who is responsible for making medical decisions in the event that you become incapacitated has become a common thread for communication throughout many different families. Many people are also exploring new financial opportunities including side jobs as a result of the uncertainty and significantly changing job market brought about by the pandemic.

A recent survey completed with nearly 2,000 Americans found that 41% of respondents saw a reduction in their work hours that impacted their income, nearly 17% were furloughed and just over 28% had lost their jobs.

The study looked at the many ways in which those people have attempted to pivot or respond, including deferring or adjusting essential payments, tapping into savings, taking out a loan or getting a side job. Now is a good opportunity to schedule a consultation with an experienced estate planning attorney to learn more about protecting your interests.

The federal exemption for estate taxes in the United States is very generous, to the point that many people assume that they do not have enough assets to be worried about estate planning. In 2020, that threshold is $11.58 million per individual. You might think that estate planning therefore only applies to the extremely wealthy.

However, there are three reasons why thinking this way is problematic and why you might want to reconsider your frame of reference in deciding to move forward. First of all, you could become wealthier, particularly if most of your current wealth is in stocks. The government could also update the rules and limits for estate tax exemptions in coming years, and finally, some states have an inheritance tax.

This is particularly important for you if you currently live in a state that does not have and inheritance tax but are thinking about retiring in a state that does.

Regardless of where you’re at in your life, you need the benefit of estate planning to help you accomplish your goals and protect those you care about. Putting together an incapacity planning plan can help you get the peace of mind that if something happens to you and you become unable to speak for yourself that there’s a plan in place to ensure you get the care and support you need.

Schedule a consultation with a knowledgeable estate planning lawyer to walk through your options and make sure you’ve thought about estate planning the right way. Our office is here to help you review an existing estate plan or to create new documents and strategies.

Small business owners have plenty of things to think about in the wake of a worldwide pandemic that has shaken many things up. But that doesn’t mean you can afford to neglect the importance of proper estate planning or business planning options. Using this time to take a step back and reorient where you want the company to go in the near future is a good way to keep on top of these important tasks and ensure that if something happens to you, there’s a plan in place.

Every business owner has the long term vision and goal that their company is a big success, but it can take a lot of work to get there and even more work to sustain it after the fact. When you need to make a departure from the company, you need to know that you have a succession plan that will serve your needs and give your business the sustainability it needs.

That comes down to systems, a succession plan, and the right people. All of these elements should be in place well before anything happens involving you or another company owner needing to make an exit. One primary reason to engage in business succession planning beyond these basics is that if you’re in a partnership, you can ensure maximum options for the remaining partner should something happen to the other one.

Buy-sell agreements can help to accomplish this task because it ensures that unless intended, the family members of the deceased party are not the ones who get access to the company value. If there’s no buy-sell agreement in place, the business could be tied up in the estate administration if one of the partners of the company passes away. Most buy-sell arrangements for small businesses will automatically allow other owners to purchase the owner’s share in the company, allowing for a smooth transition to what the business looks like in this new iteration.

Are you stuck on how to make the most out of small business estate planning? Now is a good time to discuss all your options with a dedicated business succession planning attorney in NJ. Set up your meeting today.

The world is changing, this crisis has cemented the dominance of a handful of very large technology companies (FAANG – Facebook, Amazon, Apple, Netflix, Google). Why shouldn’t investors just focus on them?

Investors may be surprised to learn that it is not unusual for the market to be concentrated in a handful of stocks, but keep in mind that any expectations about the future operational performance of a firm are already reflected in its current price.

Tech standouts are drawing attention for their perceived sway on stocks, but history undercuts that view.

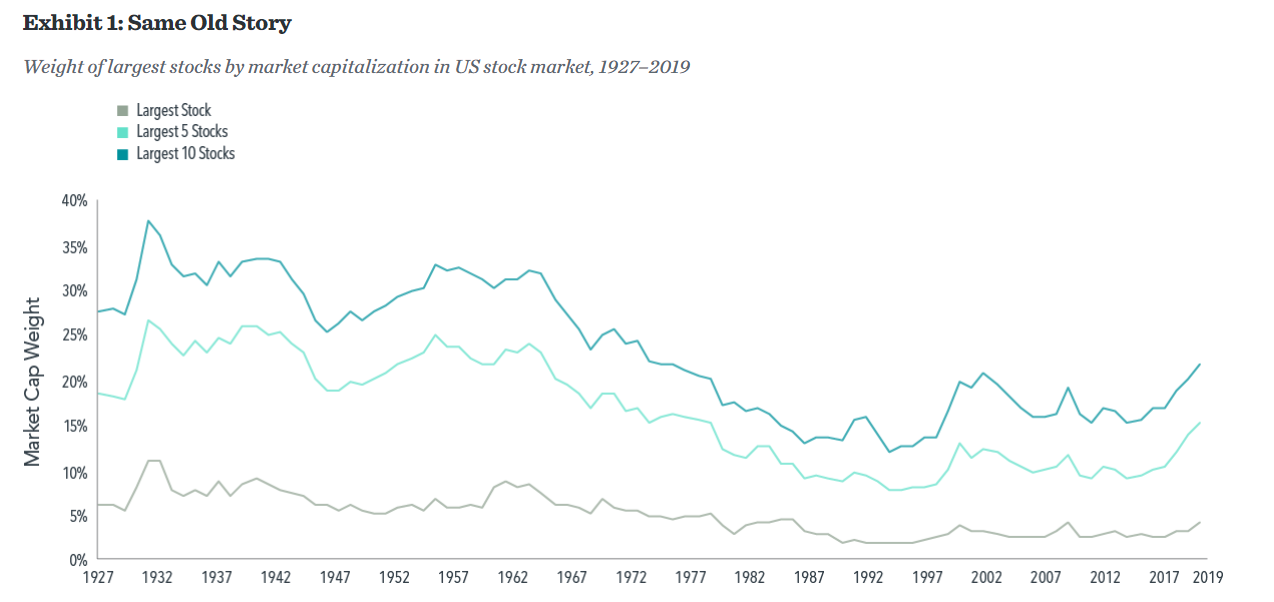

A top-heavy stock market with the largest 10 stocks accounting for over 20% of market capitalization and a marquee technology firm perched at No. 1? This sounds like a description of the current US stock market, dominated by Apple and the other FAANG stocks,1 but it is actually a reference to 1967, when IBM represented a larger portion of the market than Apple at the end of 2019 (5.8% vs. 4.1%).

As we see in Exhibit 1, it is not particularly unusual for the market to be concentrated in a handful of stocks. The combined market capitalization weight of the 10 largest stocks, just over 20% at the end of last year, has been higher in the past.

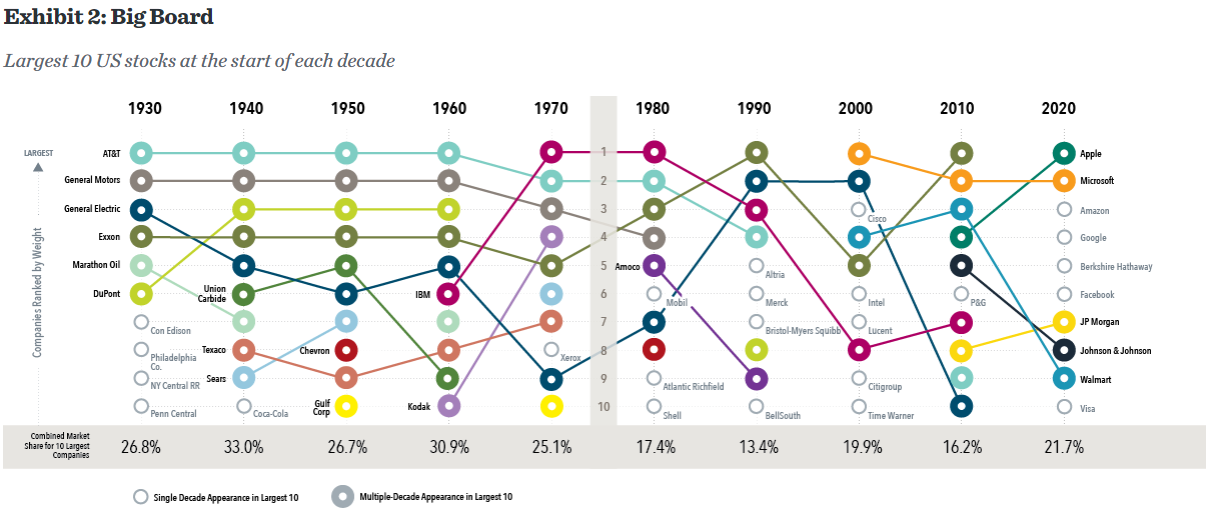

A breakdown of the largest US stocks by decade in Exhibit 2 shows some companies have stayed on top for a long time. AT&T was among the largest two for six straight decades beginning in 1930. General Motors and General Electric ranked in the top 10 at the start of multiple decades. IBM and Exxon were also mainstays in the second half of the 20th century. Hence, concentration of the stock market in a few large companies such as the FAANG stocks in recent years is not a new normal; it is old normal.

Moreover, while the definition of “high-tech” is constantly evolving, firms dominating the market have often been on the cutting edge of technology. AT&T offered the first mobile telephone service in 1946. General Motors pioneered such innovations as the electric car starter, airbags, and the automatic transmission. General Electric built upon the original Edison light bulb invention, contributing to further breakthroughs in lighting technology, such as the fluorescent bulb, halogen bulb, and the LED. So technological innovation dominating the stock market is not a new normal; it is an old normal too.

Another trend attributed to a new normal is the extraordinary performance of FAANG stocks over the past decade, leading some to wonder if we should expect these stocks to continue such strong performance going forward. Investors should remember that any expectations about the future operational performance of a firm are already reflected in its current price. While positive developments for the company that exceed current expectations may lead to further appreciation of its stock price, those unexpected changes are not predictable.

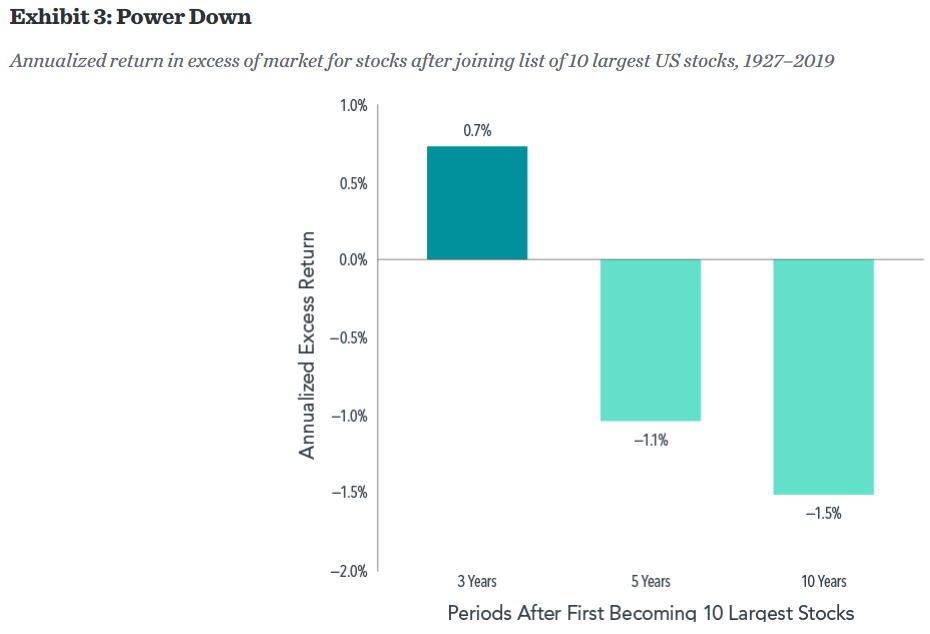

To this point, charting the performance of stocks following the year they joined the list of the 10 largest firms shows decidedly less stratospheric results. On average, these stocks outperformed the market by an annualized 0.7% in the subsequent three-year period. Over five- and 10-year periods, these stocks underperformed the market on average.

Past performance is no guarantee of future results.

The only constant is change, and the more things change the more they stay the same. This seems an apt description of the dominant stocks atop the market. While the types of businesses most prominent in the market vary through time, the fact that a small subset of companies’ stocks account for an outsized portion of the stock market is not new. And it remains impossible to systematically predict which large companies will outperform the stock market and which will underperform it. This underscores the importance of having a broadly diversified equity portfolio that provides exposure to a vast array of companies and sectors.

Sources: Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

Original article can be found at https://us.dimensional.com/perspectives/large-and-in-charge-giant-firms-atop-the-market-is-nothing-new

Americans are living longer than ever but that doesn’t always mean a longer quality of life. A proper elder care plan should account for not only having the right people in the right roles in order to make the proper financial & health Care decisions, but also guidance and direction with respect to your wishes should you not be able to speak for yourself.

When should one look for an Elder Care Attorney?

There is not an exact time when one should look for an elder care attorney but I see it most commonly when one is considering retirement, most commonly in the late 50s and onward. The need for elder care planning evolves from a properly structured financial plan & estate plan. Another way to regard it is as “Estate Planning with a very specific purpose.” If estate planning is most often is associated with ‘death planning’, then elder care planning is more ‘life & longevity planning.’

How does one choose an Elder Care Attorney?

The ideal way to choose an elder care attorney is by speaking with him or her. Referrals can be extremely helpful, as are testimonials. Credentials, such as Certified Elder Law Attorney and other such designations are helpful – but those are often an indication of standardized exams, experience, an ongoing continuing legal education & a commitment to the practice. Not to diminish those very important aspects – but elder Care planning is a personal endeavor. Traditionally, Estate Planning and Elder Care planning was done with a cookie cutter-like approach. But it’s important that the attorney who guides you on this level of planning emphasize customized solutions and listens to you. Although your pattern and your facts might be similar to others, every family has unique and deserves to be treated as such.

What should one expect when dealing with an Elder Car Law Firm?

When working with an elder care attorney, you should expect to be heard, and to have conversations. Much like going to a physician who needs to have x-rays, MRIs, lab work, etc prior to guiding you on your health needs, an Elder Care attorney is going to need baseline information with respect to your finances, health, family situation, goals and concerns, among other aspects. Be prepared to be open and forthcoming. You wouldn’t hesitate to tell your doctor if you are taking medications that may have contraindications & adverse effects – treat elder Care attorney with the same manner if you desire proper, effective advice.

Anything else I should know?

It’s important to know that Elder Care attorneys typically handle only the legal aspect of planning. However your elder care plan needs to be integrated with your financial plan, investment plan, tax plan, long-term care plan, and insurance plan. Not all attorneys are going to be equipped to handle all of these services in-house. At Shah Total Planning I handle them in-house because my clients prefer that integrated, one-stop shop. But if you can’t find somebody who does it all in the house, it’s important to find someone who is willing to communicate with your team of professionals.

When I’m speaking with a client regarding their Estate Planning, and we are discussing their Will specifically, I encouraged them to think of the Will as a recipe:

If I was going to write a recipe for a cake which required one to get the milk, sugar, eggs, etc. from various places, then blend them in a certain way, then put the mix the oven that’s been preheated, and follow the rest of the instructions – will they get a cake at the end if they follow the recipe properly? Yes.

What if I inserted instructions in the recipe that they must hop on one leg while they are mixing the ingredients? Is that going to be enforced? Will that play into the desired outcome of having a cake? Probably not. One can regard certain provisions is a Will in a similar manner.

VIDEO: What can frying eggs teach you about Wills, Trusts and Asset Protection?

If there are specific steps you are seeking for someone to take when carrying out your wishes or conditions to be met – you’re probably better off looking at a trust (bake the cake now, instead of leaving behind a recipe.) It allows you much more flexibility and control.

Remember a Will is a public record document once somebody passes away. The Will doesn’t have any “power” until it goes through probate. At that point the Will would be submitted to the surrogates court and the executor is given the appropriate documentation to carry out the wishes.

VIDEO: What is the difference between a “Will”, a “Living Will”, and a “Living Trust?”

That means having a provision such as “everything goes to my spouse as long as they don’t get remarried” would then be part of the public record. That may not be your intention.

But even beyond that – most courts will generally try to find ways to NOT enforce provisions if they are deemed to be against public policy, such as discouraging marriage.

Also, circumstances may make those restrictions inconsistent with your ultimate wishes. What if you had a provision that said a grandchild will only receive an inheritance upon receiving a degree from a four-year college institution, but then that grandchild is diagnosed with a learning disability or another condition which makes it impossible for that condition to be met? Is that consistent with the grandparents planning objective? Possibly not. But to undo that might require Court approval or even a challenge.

I don’t have an exact percentage as to how many Wills get challenged versus how many Trusts get challenge, but I would wager that it’s at least 5:1 if not 10:1 with Wills being challenged much more often.

That’s not to say you shouldn’t have specific incentive provisions or conditions which are consistent with your wishes in your Wills. However, your attorney should guide you as to whether or not there is a potential challenge looming due to either ambiguity in your desires or a difficulty in enforceability.

Challenges can be costly, but attorneys generally make more money when litigating Will disputes than they do simply administering trusts or properly carrying out the intentions in a Will. Therefore, much care should be taken in ensuring that the will is clear, enforceable, with as little complication as possible to carry out your wishes.

There is great news for clients with certain family members or other beneficiaries – this year brought with it a huge change in the law that benefits beneficiaries who are disabled or chronically ill. The Setting Every Community Up for Retirement Enhancement (SECURE) Act was integrated into the Further Consolidated Appropriations Act of 2020. The SECURE Act has been big new in the special needs planning community, as it carved out special considerations with regard to inheriting retirement accounts for those beneficiaries who are classified as disabled or chronically ill.

Before the change in the law, almost any individual could inherit a retirement account and stretch the distributions from that account over their life expectancy. That would allow the funds to be able to sit in that tax-deferred account and accumulate wealth, with the exception of a required amount that must be distributed each year. However, the SECURE Act drastically decreased which individuals would be eligible to stretch distributions over their life expectancy. Beneficiaries who are now not entitled to a stretch must withdraw the funds within either 5 or 10 years, which doesn’t allow for those funds to keep growing. But under the new rules of the SECURE Act, one category of individuals who are still entitled to the financial benefit of stretching distributions from the account over their life expectancy include beneficiaries of the retirement account who are disabled or chronically ill. So, this is a huge benefit and advantage for those disabled or chronically ill beneficiaries, possibly over other beneficiaries you may have.

In response to the new law changes, a special trust has been created to best provide for these beneficiaries. The purpose of this unique SECURE Supplemental Needs Trust is to provide for the maximum benefit of the law for disabled or chronically ill beneficiaries.

· The trust allows retirement account benefits to receive a maximum stretch under the law. This means that the beneficiary can stretch the distributions from that retirement account over their life expectancy. This allows those funds in the retirement account to keep accumulating and growing.

· The SECURE Supplemental Needs Trust also allows the beneficiary to benefit from the retirement account proceeds while still being eligible for public benefits, such as Medicaid or Supplemental Security Income.

· The trust allows for a care manager or advocate, so that someone can always be looking out for your beneficiary after you have passed.

· The trust provides for asset protection from creditors, divorce, or other bad actors.

· The trust gives you peace of mind knowing that your beneficiary will be taken care of for years to come.

If the following applies to you, then you might benefit from this new law and new SECURE Supplemental Needs Trust:

· You have a loved one or another beneficiary who is disabled or chronically ill.

· You have a retirement account, such as a 401k or IRA.

· You want to make sure that your retirement account receives maximum tax advantages after your death.

The time to plan is now. Regardless of who your beneficiaries are, you need to ensure your estate plan is up-to-date in light of the new SECURE Act. Contact our office to schedule an appointment to see how to best make the new rules work in your favor.

Going through a divorce is difficult and it shakes up your family structure and even your day-to-day life in a big way. There are also so many legal issues that have to be handled to dissolve the marriage and allow you to move on with your own life, such as moving into a new place to live or updating your last name if you had previously taken the last name of your spouse.

Some marriages might end quietly, leaving you to think that you have handled all of the most important issues from a legal perspective and are able to move on successfully into your new life. However, you need to think carefully about the importance of planning and updating your estate following the divorce.

Without a spouse through whom you can anchor your estate plan, guardians, executors, trustees and agents under health care proxies and power of attorney must be reconsidered and formally updated in your documentation. These are not the only type of documents that need to be evaluated and carefully handled in the wake of a divorce. This is because separate documentation under beneficiary forms take priority outside of any wishes you make in your estate plan.

For example, beneficiary forms associated with your life insurance policy or retirement plans must be updated to reflect the dissolution of the marriage, otherwise these are legally binding and you most likely have your spouse listed as the recipient of these accounts. Make sure that you review your marriage dissolution documents to determine some of the steps you need to take. Provisions inside these agreements might call for the removal of spouses from one another’s estate planning documents and retirement accounts but it falls to you to make sure that this is carried through.

When planning ahead for the future of your estate, trust administration and probate administration are not one and the same. There are some key differences between administering a trust estate and administering an estate inside probate.

The most important difference, for example, is that trust administration is private. For trust administration to begin, a notice letter should be sent to decedent’s beneficiaries and heirs informing them that the trust is being administered. Probate, however, is supervised by the court.

During probate, any of the documents related to the will become subject to public record. This means that details of the estate could be accessed by any member of the public who requests them. Probate will also apply if there is no will and the same rules of public record apply. In terms of trust administration, however, only the trustee and the heirs are able to see the details of the trust.

Another difference between these two processes is that the expenses are different. With probate, you need to submit a court filing fee and any fee associated with publicizing the estate in the newspaper. Any personal representative fees would also be covered under the overall value of the estate’s assets.

For trust administration, the trustee is still entitled to reasonably pay for his or her services, but there are no court filing fees. Unless there is a contest over the trust itself, there’s unlikely to be too many other costs associated with administration or dispute.

Depending on your individual goals, you might need both a trust and a will.

Do you have questions about using both a trust and a will for your estate planning in New Jersey? Our law office is still here working with clients actively and helping them determine their next steps. Schedule a consultation with our law firm today so that you can learn more about what to do next.