A total of 22% of today’s population includes the baby boomer generation. Many of them are quickly reaching retirement age raising important questions about the value of estate planning.

Estate planning is so much more than passing along possessions and assets to millennial children. It is also about protecting their lifestyles and taking a long-range view towards the need for possible Medicaid support or other long-term care planning. The youngest baby boomers are turning 56 in 2020 and many of them have wealth that is expected to grow in the coming decades.

Plenty of these baby boomers might not consider themselves wealthy outright but having a home, a second property, a car or money set inside a savings account means that you can still benefit from the strategies provided by an estate planning attorney.

This is because estate planning is more expansive than determining what happens to your possessions when you’re no longer around. It takes into account your individual decisions and preferences around long term care and health care. Schedule a consultation today with a knowledgeable estate planning attorney to discuss how this can fit into your plan as a baby boomer.

Our law office is still open but helping our clients over the phone and virtually. Don’t hesitate to reach out to determine how we can help you connect your estate plan, your elder law plan, and your retirement plan.

No one could have foreseen or

wished for this Pandemic, or the impact that it has had on our planet. Yet one

of the silver linings of all the current events has been the compassion and

willingness that humanity has exhibited in helping one another. The amount of

kindness, charitable gifting & volunteer work has been tremendous, and it

is quite different than it was prior to the Pandemic.

Specifically, under the CARES act passed earlier this year, there are several changes to the way gifting is done to charitable organizations.

To start, there is now a $300 deduction available for Charitable Gifts to qualified organizations, even if you’re not itemizing your tax deductions. That is a change from the current law. It’s not clear whether this will continue beyond 2020, but it has certainly made it easier to obtain a tax benefit as a result of the gift.

Also, there is a suspension for tax year 2020 of the rule that requires you to limit your charitable deduction to 60% of your adjusted gross income – no matter how much you’ve gifted. There seems to be no limit in 2020.

Gifting for Retirees has taken on a different angle as well. Because of the suspension of the rule that requires retirees to take Required Minimum Distributions from their Qualified retirement accounts, retirees might be less incentivized to utilize the Qualified Charitable Deduction tool which allows them to gift directly to a charity from retirement accounts such as and IRA and 401k (thereby reducing potential tax liability.) Although that rule is still an acceptable method of gifting, and should still be considered when gifting above the $300 amount.

Unfortunately situations like this also bring out the worst in some people. That also means that scammers and those with less altruistic intentions can take advantage of generosity. Two tools which can be used to investigate whether or not a charity is in fact a legitimate charity and determine whether or not is properly formed for tax purposes are (a) the IRS website and (b) the Charity Navigator website. Specifically under the IRS website you can do a search to see whether it is a tax exempt organization.

It’s important to set the expectation at the onset whether or not you are expecting to receive a tax benefit as a result of your charitable gift. It’s not always the case that the donor is seeking tax benefits. However, if a tax benefit (deduction) is sought, best to confirm that it is a 501 (c) (3) organization & obtain proper documentation of the gift.

Checking on some smaller charities & grassroots organizations/movements is much more difficult – it’s important to know how you came across the charity – a personal connection? Social media? Or did they solicit you from out of the blue. Don’t be afraid to ask probing questions of the organizers.

Gofundme.com pages have had a tremendous impact on helping with causes, although they’re usually not for tax-exempt charities. You should know that there is minimal supervision & policing of what exactly is done with the money after it’s been collected. Again, here a personal connection to the cause and to the persons in charge of the cause is helpful to determine legitimacy.

An executive order from Governor Phil Murphy now means that municipalities can update their property tax payment deadline from May 1st to June 1st. According to research completed by The Tax Foundation, The Garden State is actually home to the highest mean effective property tax in the entire country at 2.21%.

This gives homeowners in New Jersey a little bit of breathing room in their taxes. Now is a really good time to evaluate your current tax obligations across the board.

Do you have appropriate tax planning strategies in place to protect your estate as well as taking into consideration the possibility of needing long term care in the future? Schedule a consultation with an experienced New Jersey estate planning lawyer if you have more questions about the best way to protect your interests.

Do you have planning in place for what will happen to your property if something happens to you? Do you own other real property either in New Jersey or in a different state? You need to plan for this as part of your asset transfer strategy.

Tax strategy planning can go a long way in helping you to avoid problems and potential disputes down the line. When your estate enters the probate process, the work you’ve already done in terms of planning will help your family members during this difficult time and ensure a smooth transfer of your property using the tools you’ve already outlined.

Schedule a consultation with a lawyer who is very familiar with state and federal taxes and how they fit into the bigger picture of your estate plan.

An important part of owning a successful business isn’t just documenting what you do now that makes you effective but also outlining a plan for what happens when you decide it’s time to move on or are forced to move on for circumstances outside your control.

Do you already have a successor lined up who can make the difficult decisions that you have made in the past? The next in line person to take over your role and take the business into the future should be someone who has a big passion for the work, the expertise needed to leverage business longevity and the willingness and ability to work with other employees.

Far too many small and medium sized businesses fail due to a lack of

succession planning. In fact, the exit planning institute reports that 78% of

businesses have no transition team in place and nearly 83% have no written

transition plan. The employees staying in the business and the entire company

at risk.

The right succession plan will be created now before you have any intention of leaving. It helps to protect a thriving enterprise and covers the need to transfer control to a successor and the possibility of the owner’s sudden departure. Finding the right successor is a process that should begin now.

Talk to our business succession planning lawyer today to learn more

about how to begin the process. Your succession plan is there to help your

employees, your leadership team, and the company not just survive your

departure, but to continue growing and building on the firm foundation of

success you already set up.

Research shows that two out of every three Americans will need some form of assistance with activities of daily living. These activities of daily living are defined as dressing, bathing, walking, and toileting.

These activities of daily living could be impeded for an extended period

of time or for a short term. Long-term care is often associated with nursing

homes, but this is not the only way where the individuals can get support with

care. In fact, the truth is that many people who need additional assistance get

that care from home.

A long-term care plan is your big picture understanding of what you

intend to happen in your retirement years and beyond in the event that you need

long term care assistance. It is a common misconception that Medicare, the

federal program that administers health care benefits for senior citizens, will

step in to pay for long term care services on your behalf.

Medicare does not cover the vast majority of long-term care expenses and

for those who do not have a long-term care insurance policy to support them, it

falls to them to self-fund for their care. This can be especially overwhelming

and confusing for those families that are approaching the long-term care crisis

for the very first time. An elder law attorney or estate planning attorney can

assist you with crafting a long-term care plan with your individual needs in

mind.

It might feel as though everything is up in the air with your financial planning situation lately. Since this has impacts on your day to day life and your overall financial picture, it’s important to think about how any changes you make now in light of the pandemic could influence your estate planning picture.

Our estate planning law firm is here to help you evaluate

your current strategies or define your next steps for adjusting your strategy.

The IRS has been issuing guidance about issues ranging from the Paycheck

Protection Program to the ability to pull money from your IRA, but it’s up to

you to be informed about how you respond and what you do next.

As of May 2020, you can remove up to $100,000 from your IRA

so long as you pay it back within three years and take no tax hit for that

transaction. However, you might be looking at some tax issues in the interim.

The IRS has chosen to call these transactions coronavirus-related

distributions. But as with all aspects of the new programs available to

individuals and business owners, proceed with caution.

Each withdrawal and then repayment back into the IRA

is treated like a rollover transaction classified as “free.” The good news

about this is that there are no limits on what you can use the money you withdraw

for, however, you might need to file amended tax returns in order to get the federal-income-tax-free

treatment.

If your IRA was also an important component of your

retirement and estate plan, you’ll want to think carefully about what makes the

most sense in terms of how you proceed and whether pulling money from your IRA

is the right choice for you right now. If you need assistance in recalibrating

your estate plan or strategies right now, set up a meeting with our office to

discuss options- we’re still working and here to help virtually.

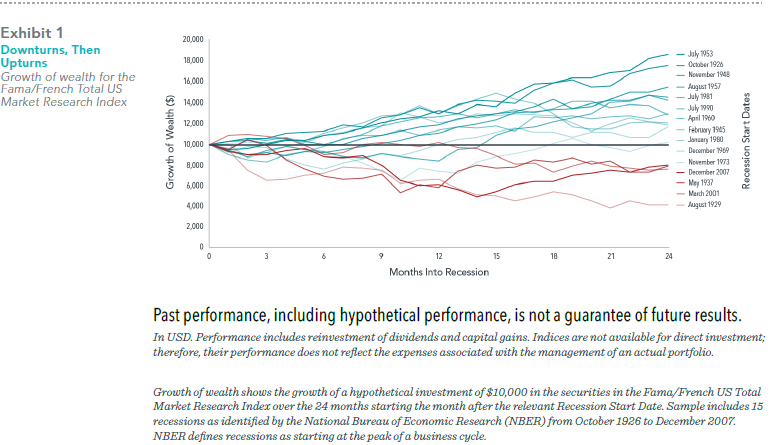

With activity in many industries sharply curtailed in an effort to reduce the chances of spreading the coronavirus, some economists say a recession is inevitable, if one hasn’t already begun.1 From a markets perspective, we have already experienced a drop in stocks, as prices have likely incorporated the growing chance of recession. Investors may be tempted to abandon equities and go to cash because of perceptions of recessions and their impact. But across the two years that follow a recession’s onset, equities have a history of positive performance.

Data covering the past century’s 15 US recessions show that investors tended to be rewarded for sticking with stocks. Exhibit 1 shows that in 11 of the 15 instances, or 73% of the time, returns on stocks were positive two years after a recession began. The annualized market return for the two years following a recession’s start averaged 7.8%.

Recessions understandably trigger worries over how markets might perform. But history can be a comfort for investors wondering whether now may be the time to move out of stocks.

GLOSSARY Fama/French Total US Market Research Index: The value-weighed US market index is constructed every month, using all issues listed on the NYSE, AMEX, or Nasdaq with available outstanding shares and valid prices for that month and the month before. Exclusions: American Depositary Receipts. Sources: CRSP for value-weighted US market return. Rebalancing: Monthly. Dividends: Reinvested in the paying company until the portfolio is rebalanced.

_______________________________________________

Nelson D. Schwartz, “Coronavirus Recession Looms, Its Course ‘Unrecognizable,’” New YorkTimes, March 21, 2020; Peter Coy, “The U.S. May Already Be in a Recession,” Bloomberg Businessweek, March 6, 2020.

_______________________________________________

Sources: Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

When you appoint another person to make decisions for you that are legally binding, you need to use a power of attorney to establish this authority. The person you empower is referred to as an attorney-in-fact. There are many different kinds of powers that can be given to this person, and the most common ways to use such a document include giving them authority for your medical decisions or your financial choices.

However, you can decide with your lawyer what makes the most

sense in terms of giving powers to your attorney-in-fact. Tailoring the POA to

work for you means thinking about whether or not you have other things you’d

like to be able to pass on to this agent.

You can specifically name the kinds of things you’d like

this agent to be able to do, such as:

Paying for a child’s medical expenses or college

tuition

Hiring a repairman to fix something on your

property

Handling government benefits or filing for taxes

Exchanging, purchasing, or selling certain goods

Giving to charities with your assets

Handling the management of your existing

insurance policies

Accepting benefits and changing retirement plans

You can make your power of attorney document as specific or

as broad as you choose. The important thing is that you have a lawyer review

this document and walk you through the benefits or potential challenges of the

way you’ve laid it out. This will give you clarity and the chance to update or

adjust things as needed.

Not everyone can be an attorney-in-fact. This person must be

classified in your state as an adult, should not be someone who is filing for or

waiting approval for a bankruptcy discharge, and not the owner or employee of a

nursing home where the principal (the person creating the document) is a

current resident. It’s a good idea to select someone who is comfortable serving

in this important role and someone who you trust with your affairs.

Have more questions about the process of creating and

implementing a power of attorney? Speak with a lawyer today about your options.