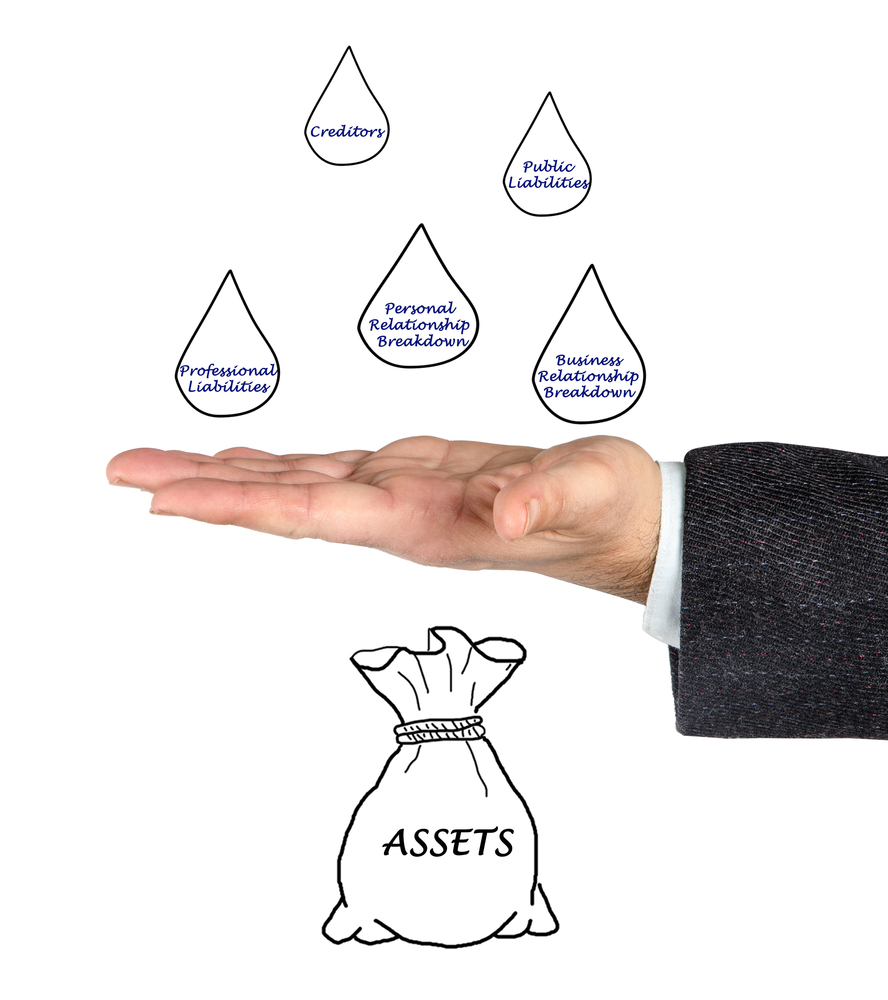

Part of estate planning is ensuring that the inheritance you pass on goes where you want it to after your death. But how can you ensure that your assets are protected long after you’re gone? Do you hope to pass on as many assets as possible? Do you know whether or not your beneficiaries could be exposed to risks that could cost them all of the assets you’ve worked so hard to build? In an increasingly litigious environment, proper asset protection planning using tools like trusts is a must.

People focus on avoiding probate and putting together a will during estate planning, but it turns out you may need more comprehensive strategies than that. If you died prematurely, became incapacitated, are involved in a rocky marriage that suddenly ends in divorce, or are sued in the next month, all of these are potential attacks on that inheritance you’ve worked so hard to build.

One opportunity to protect this is to use an appropriate trust. This means that there is a clear set of instructions inside the trust about when assets can be removed, such as for education and medical expenses. This can help to guard against the inheritance being squandered. Many people choose a trust because it gives an additional layer of control and peace of mind in the event that you were to become incapacitated or pass away suddenly. It is critical to have a plan in place to protect an inheritance from interference from outside threats, because unfortunately, many people minimize the likelihood of these outside threats.